“Health care should be a right, not a privilege, and Americans facing illness should never have to worry about how they are going to pay for their treatment.” Thus begins the Joe Biden White House’s description of the signature health care investment in their American Families Plan (AFP).

Unfortunately, that proposed $200 billion investment in no way matches the rhetoric. The AFP makes the expanded health care subsidies in the recently passed American Rescue Plan (ARP) permanent, but these expanded subsidies serve primarily to funnel money into insurance executives’ pockets while only making health care somewhat more affordable for millions of people in need. As policymakers debate their next steps forward on health care, it is essential that Democrats take a more critical look at one of Obamacare’s worst elements.

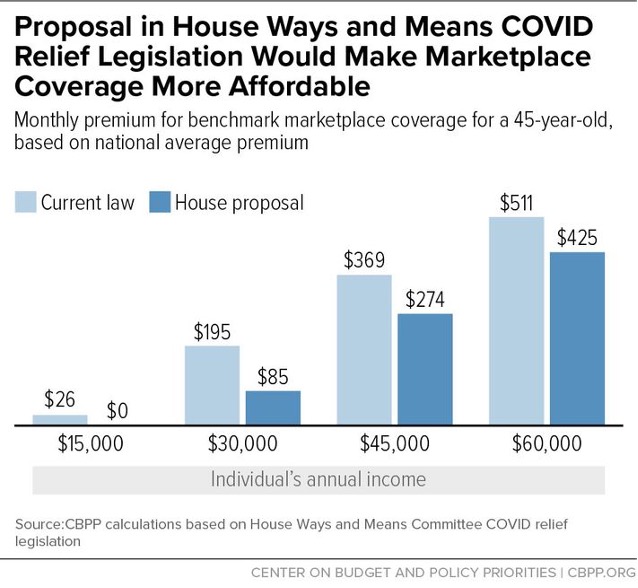

Health policy analysts typically focus on monthly health care premiums as the primary indicator of health plan affordability. In a February column excitedly touting the ARP’s temporary subsidy improvements, for example, New York Magazine’s Jonathan Chait included the graph below from my former colleagues at the Center on Budget and Policy Priorities (CBPP). It shows that the new subsidies should be saving people making between $30,000 and $60,000 roughly $100 per month on their premium payments.

Unfortunately, these types of graphs miss what’s really happening with health care affordability. On the most basic level, by plotting monthly premium amounts against annual income, they make it seem like premiums are much more affordable than they really are. $274 per month doesn’t sound nearly as bad as $3,288 per year, which is how much a typical 45-year-old individual making only $45,000 a year will continue to be expected to hand over to their insurance company if the AFP becomes law.

More importantly, these graphs omit the significant amount of additional money it takes for low- and moderate-income people to actually access the care their premiums are supposed to cover. Deductibles in particular are incredibly high on the Obamacare exchanges. The average deductible for a benchmark (Silver) plan on the exchanges is $4,800, meaning that, if the aforementioned 45-year-old got sick and needed $4,800 worth of care, the insurance company would not chip in at all. So that individual would end up paying $4,800 for their care in addition to $3,288 in premiums to the insurance company – or 18% of their income in total. If the individual’s health care costs exceed the amount of the deductible and the individual receives care from an in-network doctor – which is hardly a guarantee – the insurance company will begin to contribute. But even then, the individual will be on the hook for additional “co-pays” or a percentage of the additional costs due to “coinsurance.” Americans facing illness should never have to worry about how they are going to pay for their treatment, but if they have a new and improved Obamacare exchange plan they’d still be crazy not to worry. And they will continue to decline needed care because they cannot afford the deductibles and/or coinsurance.

In addition to ignoring the continuing health care accessibility problems faced by many individuals, common analyses of the increased subsidy approach fail to show the massive amounts of money being funneled from taxpayers to the insurance industry. Expanded subsidies mean individuals pay less to the insurance company but the government pays more.

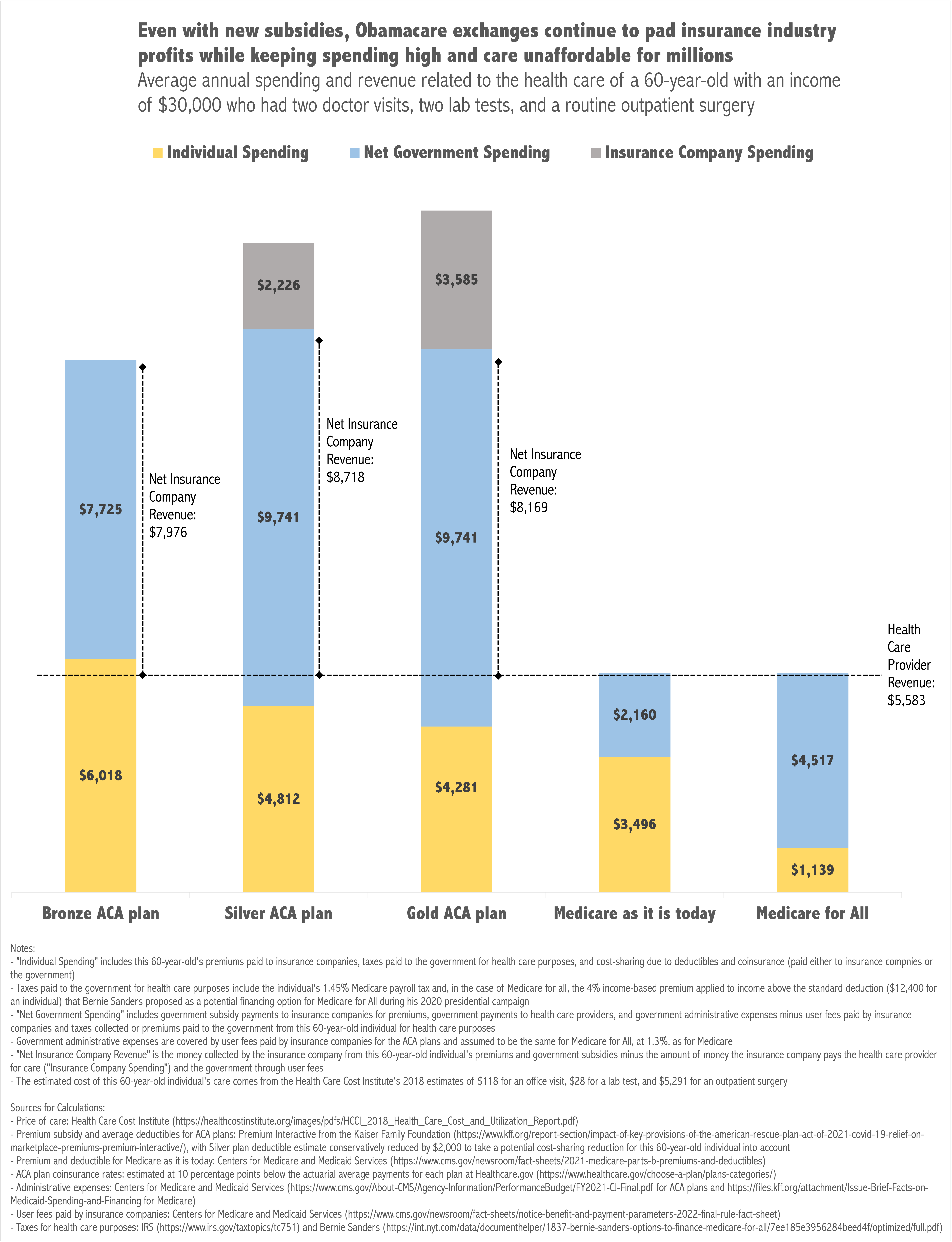

The graph below addresses all of these problems. It shows health care spending and revenues for a 60-year-old individual making $30,000 who requires some medical care during the year – two doctors’ visits beyond the physical Obamacare covers, two lab tests, and a routine surgery, the combined price of which can be estimated at $5,583 – under five different coverage scenarios. The first three scenarios are coverage under an average Bronze, Silver, or Gold plan that this individual would have access to today (with the enhancements in the ARP that the AFP seeks to make permanent factored in). The fourth scenario is coverage under the Medicare program, which 17 senators and 156 House Democrats recently asked Biden to improve and extend to individuals below age 60. While Biden and Democratic leadership have yet to indicate they will actually do that, the White House does claim in both their AFP Fact Sheet and budget writeup that, in the words of the budget document, Biden “supports…giving people age 60 and older the option to enroll in the Medicare program.”

The fifth and final scenario is coverage under the Medicare for All proposal that was a centerpiece of Bernie Sanders’s presidential campaign. Medicare for All legislation in both the Senate and House of Representatives has numerous cosponsors. Biden and congressional Democratic leaders remain opposed to this policy, however.

Each bar in the graph has three potential components: individual spending (yellow), or how much the 60-year-old spends on health care taxes (they would have to pay the 1.45% Medicare payroll tax under each scenario, which would come out to $435 annually), premiums, and payments to their health care providers; net government spending (blue), or how much the government spends in payments to the individual’s insurance company and health care providers plus administrative expenses minus the fee the government charges the insurance company to sell insurance on the exchanges and the health care taxes and/or premiums the individual pays to the government; and insurance company spending (gray), or how much the insurance company ends up paying to the individual’s health care providers on the individual’s behalf.

The dotted lines show overall health care spending and who receives the revenue. The horizontal line shows what the health care providers receive in every scenario: $5,583, which is the cost of the care itself. The vertical lines show net insurance company revenue, or how much the insurance company takes in from the government and individual from premiums and subsidies minus the fee the company pays the government to sell on the exchanges and what the company actually contributes towards the individual’s care.

As the graph shows, the Obamacare plans are a disaster for both this relatively healthy 60-year-old and the government. The new subsidies in the ARP actually bring the average Bronze plan premium for this person down to $0 annually, but the average Bronze plan’s deductible of $6,900 means the individual must pay for the full cost of care themselves (assuming they do not forgo the needed care because of the cost), bringing their total health care expenses (including Medicare payroll taxes) to over 20% of their income. The government, meanwhile, pays the insurance company an annual premium of $8,160 through the Obamacare subsidies – far more than what the care itself costs and netting the insurance company $7,976 after subtracting their $184 user fee – in order for the insurance company to contribute nothing at all!

Silver plans are typically considered the best value on the exchanges, in part because lower-income individuals who buy Silver plans can qualify for some cost-sharing reductions. The amount of those reductions vary, but let’s assume this individual buys a plan with a sizable reduction that takes their deductible down $2,000 from the $4,800 average. Co-pays and coinsurance also vary plan to plan, but one of the better Silver plans might cover 80% of costs above the deductible. So once the $2,800 deductible is exceeded, the insurance company in this case would pay $2,226 of the remaining $2,783 the individual owes. Yet between the individual’s $1,020 annual premium payment to the insurance company, Medicare taxes, and $3,357 payment to their health care providers (due mainly to their still-large deductible), they would still be paying close to $5,000 towards health care – which someone making $30,000 a year obviously cannot afford. The government’s subsidy payment to the insurance company would be even larger than it was for the Bronze plan – $10,176 for the year – and the insurance company would pocket $8,718, which would once again be far more than the cost of care itself.

The average Gold plan, with a deductible of “only” $1,600 and coinsurance that might be 10%, is the best plan for an individual needing care. But with an annual premium of $1,848, the $1,600 deductible, and a $398 coinsurance payment above the deductible, our example 60-year-old making $30,000 a year would still need to pay over 14% of their income towards health care costs. The insurance company would contribute $3,585 towards care in this scenario but would still net a tidy $8,169 in revenue.

With government insurance the situation is radically different. Medicare Part B requires individuals at this income level to pay premiums comparable to those under the Gold plan, or $1,782 annually, and also has 20% coinsurance. But the deductible is only $203, saving our hypothetical 60-year-old $785 relative to the Gold plan. The biggest difference is that there is no massive subsidy for the government to pay to the insurance company in this scenario; administrative expenses are negligible (only $73) and American taxpayers collectively save thousands of dollars that would otherwise be wasted on insurance company executives’ outrageously high salaries. There’s really no justification for the Obamacare subsidies approach relative to the expansion of Medicare approach unless your goal is to pad insurance company profits.

Medicare for All would result in slightly-smaller-than-for-present-day-Medicare-but-still-major taxpayer savings relative to the Obamacare approach and, most importantly, is the best deal for the individual needing care. Our 60-year-old friend’s taxes would increase somewhat (by $704) under the income-based tax proposal Sanders released as one of a variety of potential Medicare for All financing options, but that tax increase would be more than offset by eliminating premiums, deductibles, and coinsurance. This individual would pay less than 4% of their income towards health care costs regardless of what care they needed. They would not “have to worry about how they are going to pay for their treatment,” which is why Medicare for All is the clear choice for everyone who truly believes that “health care should be a right, not a privilege.”

Leave a comment